By Colin Savage. (@prestwichblue)

Introduction

I’ve written about this before but it’s clear some people still think that it’s something that I’ve made up in my fevered imagination. Having revisited what I have written, I realise I haven’t actually done chapter and verse on this previously, so in the light of recent events, I’m going to revisit this and put it to bed once and for all.

I’m going to show, this time with actual figures and step-by-step calculations as detailed in UEFA’s own FFP documents, how there was a change to a key rule between City’s 2012 accounts being filed (the first under FFP) and the first assessment period in 2013/14. I’m also going to demonstrate how that changed the picture for City completely. It should also answer the question of why City were allegedly inflating sponsorship deals above market value, as detailed in Der Spiegel.

With aggregate losses of over £150m in those first two years to be assessed, when the maximum allowable loss was around £38m (€45m), City were way off being able to pass FFP. But they were, in my view, planning to use a specific provision, added as Section 2 to Annex XI in the FFP rules, to avoid sanctions. Annex XI is part of the formal FFP regulations and details factors to be considered when assessing compliance with the break-even requirement. That plan by City obviously failed, as they did suffer a set of sanctions, but I’ll show how I believe that happened.

My claim that City were planning this, is backed up in three separate statements. In the first, issued at the time the sanctions were made public, the chairman said that there had been a “fundamental disagreement” between City & UEFA over the calculation of 2012 wages paid under contracts signed before June 2010. It’s quite amazing that no one picked up on this and asked City to explain.

The others involved emails used in the Der Spiegel articles, which weren’t in the public domain at the time. There’s one where Chief Finance Officer Jorge Chumillas said, “We will have a shortfall of £9.9m in order to comply with UEFA FFP this season.” City needed much more than that to comply with FFP (over £75m as I’ll show shortly) so why was he so worried about £10m?

There was another email, where Finance Director Andrew Widdowson is alleged to have said “We are breaching anyway. We are just relying on mitigating factors to get us through.” That was spun by Der Spiegel as a desperate admission that City had given up trying to beat FFP – when, as I’ll demonstrate, the need to use mitigating factors was always the plan. It couldn’t have been anything else.

FFP & Annex XI

Why was this crucial to City’s hopes of getting past FFP sanctions? FFP requires clubs (among other things) to balance income and expenditure. The largest item of expenditure in most football clubs’ accounts is player wages. In 2012, for example, it made up over 75% of our total operating expenses and 87% of our total revenue. That meant for every pound we took in revenue, 87p was going towards our wage bill. Even now, with revenue of over £500m, wages make up just over 50% of that revenue and over two-thirds of our operating expenses.

When clubs sign the players they pay these wages to, they generally do that for 5 years initially and they’re committed to contracts for that whole period. Many were worried that contracts they’d signed prior to FFP being announced, might impact their ability to meet the break-even requirement. UEFA recognised this and introduced this extra, transitional provision into Annex XI as a result.

This covered the initial two assessment periods of FFP, and said that, in principle, clubs who failed FFP as a result of wages paid in the 2012 financial year under player contracts signed prior to June 2010 wouldn’t be sanctioned as a result of that failure. So, it was important to be able to meet that requirement if you knew you were likely to fail, as City were.

Let’s just review what FFP required. The first FFP assessment period was the 2013/14 season and that involved two sets of accounts; those for the reporting periods ending in 2012 and 2013. In City’s case their year-end was May at the time, so it was the accounts for the years ending 31st May 2012 and 31st May 2013. From then on it would be assessed on a rolling 3-year basis.

To be able to meet the break-even requirement, clubs had to report a break-even deficit over those first two years (defined as the bottom line loss reduced by some allowable expenses) of no more than €5m.

In addition, in the early assessment periods, an owner/investor could subsidise up to €40m of additional losses. So, if your owner was prepared to do that (and we must presume ours was) then you could sustain an aggregate break-even deficit of up to €45m in total over those two years. This is known in FFP parlance as the “acceptable deviation” and I’ll use this term from now on.

To avoid confusion over currencies, I’m going to translate that €45m as £38.5m, based on the approximate exchange rate at the time.

Here’s how it was phrased in the FFP Regulations at the time (copied directly from the document):

There were three tests in (i) and (ii) that had to be met in order to be able to claim mitigation under the above provisions in Annex XI. The wording of the first two, detailed in part (i) and the first part of part (ii) is clear;

- The club had to demonstrate a positive trend in in its break-even results, thereby proving it had a strategy for future compliance;

- The club had to demonstrate that the aggregate break-even deficit [although the wording is wrong – they mean the difference between total break-even deficit of all the financial years under review and the acceptable deviation] was only due to the deficit in the reporting period ending in 2012;

- The third test, however, is a bit ambiguous, starting at the words. “…which in turn is due to contracts with players undertaken prior to 1 June 2010…”. Does this mean that wages paid under contracts signed prior to June 2010 had to be responsible for the aggregate break-even deficit (over the 2 years assessed) or just for the deficit in the reporting period ending in 2012? It’s two different tests, which could be read either way, and this was the problem as I’ll show later.

City reported bottom line losses of £98.7m in 2012 and £51.6m in 2013, giving an aggregate loss for the two years of £150.3m. Clearly, that figure is quite a bit bigger than the acceptable deviation of a £38.5m deficit that we needed to achieve. In fact, we were nearly £112m light of that figure but there was another part of FFP that would help reduce that a little.

UEFA allow clubs to disregard expenditure regarded as “good” and that includes money spent on youth development, women’s football, community activities and some aspects of infrastructure expenses, mainly depreciation.

City, or someone who had been given the information by City, had released into the public domain the information that these costs totalled £35m for the two years under review. I’m going to split these as £17.5m in each of the 2 years. That gives us most of the figures we need so I’ll detail them:

The FFP Assessment Calculations

To avoid having to use the description of these numbers every time, I’ve labelled them figures A to J for simplicity.

As you can see, Figure J, which is the difference between our FFP-adjusted aggregate break-even deficit and our acceptable deviation, is nearly £77m so we’re still a long way from complying with the FFP break-even requirement. The £10m Der Spiegel said we were struggling to make up makes little impact on that deficit.

This is where the allowance for wages paid under contracts signed prior to June 2010 comes in though.

If we could show, according to UEFA’s three tests, that these were the difference between passing and failing then, as per Annex XI, we should avoid sanctions.

The figure for those wages was £80m I’m told. That came from Swiss Ramble, well known to those of us who follow football finance issues, who had contacts in UEFA. He had been in to UEFA HQ to speak to his contacts and this is what he was told. This was surprisingly high to both of us, but he explained that City had been able to clarify that even if a contract had been renegotiated after June 1st, 2010, the original amount of the contracts could still be included.

As an example, if we signed a contract with Player A for £100k per week in July 2009, then renegotiated it in July 2011 to £120k per week, the £100k could still be included in these Annex XI allowable wages. This had been discussed and agreed with UEFA.

Looking at Figure J, you’ll see that this £80m just covered our deficit over the acceptable deviation of £76.8m.

As I’ll show, this becomes important when we step through UEFA’s calculations.

So, let’s do it.

To aid clubs, UEFA sent out a ‘toolkit’ containing a spreadsheet template along with detailed instructions on how to complete it, including the calculation of whether Annex XI (2) could be applied. I’ve used this toolkit to show these calculations.

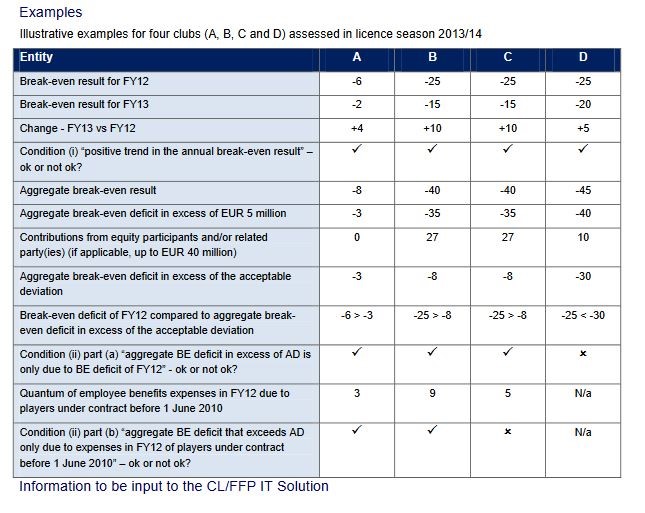

1) The 2011 Calculation

To show the steps, I’ve copied the relevant page from the UEFA document. It’s on page 70 of Version 3 of the 2011 toolkit and gives illustrative examples to aid performing the checks. This is the original version of the toolkit, initially sent out to clubs in order to record their 2012 figures in accordance with FFP regulations.

I think that the spreadsheet included with this was sent to UEFA as part of the FFP submission, even though the figures didn’t come into play until added to the 2013 figures. I will, however, include the 2013 figures in the calculation, in order to show how the crucial change to the toolkit had such an impact. This is what the club would presumably have been using when working out what financial result they needed to deliver in 2013.

Here we go.

Lines 1 & 2 are the Break-even result for the Financial Years 2102 and 2013 and equate to figures C and F above, which are the break-even deficits of £81.2m and £34.1m respectively.

Line 3 checks the change from C to F. These are deficits, so negative, and therefore a deficit of £34.1m is an improvement of £47.1m on a deficit of £81.2m.

Line 4 asks if Condition (i) (which equates to Test 1) has been met and there is a positive trend in the break-even result, meaning that first condition has been met. So, Test 1 is passed.

Line 5 requires the aggregate break-even result, which is a deficit of £115.3m (Figure G above)

Lines 6 & 7 can be combined as these relate to the acceptable deviation of €5m and owner investment of up to €40m. I think it’s safe to assume that ADUG were happy to fund that €40m, meaning our acceptable deviation is Figure H, £38.5m.

Line 8 requires the difference between the aggregate break-even deficit (£115.3m) and the acceptable deviation (£38.5m), which is our figure J of £76.8m.

Line 9 compares Figure J to Figure C and checks whether our deficit for the 2012 FY is the sole reason for our overall deficit in excess of the acceptable deviation. Figure C is a deficit of £81.2m while Figure J is a deficit of £76.8m and so we can see that that J is less than C and therefore the 2012 deficit is indeed solely responsible for the overall deficit in excess of the acceptable deviation.

Line 10 then confirms that condition (ii) part (a), which equates to Test 2 above, has been met, which it has in our case.

Now comes the final test, which relates to the wages paid under the provisions of Annex XI relating to contracts signed prior to June 2010. We’ve said that’s £80m previously so that’s the figure in Line 11.

The test in Line 12 (the one circled) is to check whether that £80m is wholly responsible for the £76.8m deficit, which is Figure J. The answer is that it is, as it’s greater than Figure J, meaning that we passed all three tests. In other words, if we had taken these wages out of the accounts completely, we would have met FFP and, in principle, shouldn’t have been punished.

I’ve used the figures from both the 2012 and 2013 accounts to demonstrate what would have been the situation had this version of the rules been applied in the first assessment period in 2013/14. But it’s not hard to work out that once City’s financial bods finalised the 2012 accounts, armed with this requirement they knew exactly what result they had to achieve in 2013. I certainly did, as I said, in a King of the Kippax article after the 2012 accounts had been released that we needed to report a loss of no more than £55m in order to be OK. And, sure enough, we did.

This explains why we were so keen to increase some sponsorships and do everything possible to hit that sub-£55m figure. We knew exactly what we had to do to get this over the line and that’s why the £9.9m shortfall mentioned by the CFO was so important. Every pound counted if we were to hit the right numbers.

But there was a problem.

City had apparently been working closely with UEFA on checking that everything they were doing was OK and that they understood the path to avoiding sanctions.

But almost as soon as the ink was dry on the 2012 accounts and they’d been filed at Companies House, UEFA released a new version of their toolkit and those calculations relating to the pre-June 2010 wages had changed. This was enough to render City’s careful planning, and any assurances UEFA had given them, null and void.

2) The 2013 Calculation

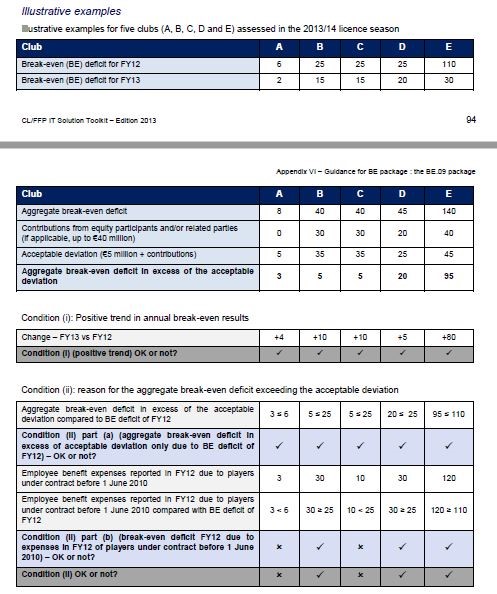

Here’s the new illustrative example from that 2013 document (pages 94 & 95).

The first parts are identical, with the same figures, so we don’t need to run through them again in detail. Suffice to say that there is still a positive trend in the financial results from 2012 to 2013 and that the aggregate break-even deficit (Fig J) of £76.8m is in excess of the acceptable deviation of £38.5m only due to the break-even deficit (Fig C) in 2012 of £81.2m.

The relevant wage figure is still £80m but the penultimate line (circled again) asks a different question to the one in the previous toolkit, to determine whether Test 3 is satisfied. It checks whether the 2012 break-even deficit only (rather than the £76.8m in Fig J) is solely caused by that £80m. As the relevant figure, Fig C, is £81.2m, the answer to that is now that it isn’t, as there are £1.2m other losses beyond the £80m wages. So, it’s a case of close but no cigar. Having been inside the original test by £3.2m, we were now outside it by just £1.2m.

Conclusion

It’s as clear as day that the test changed therefore and, using the same set of figures in both, it’s also clear that the change in that test had a crucial impact on our ability to claim mitigation under Annex XI. Had the 2011 version of the test been in place in 2013/14, we would, in principle, have avoided sanctions but the revised test meant we didn’t.

And I can’t stress enough that by changing the test to use the 2012 deficit only, after the 2012 accounts were published, there was no way back.

Had we known about it earlier, there are things we could have done to find the additional £2m or more we needed to comply with the Annex XI tests, specifically the third one.

But that avenue was closed to us. If it was a trap, it was a very cleverly laid one. On the other hand, UEFA could claim that the revised test met what they had intended to achieve in the first place.

But if you still don’t believe me on this, here’s what the highly respected blogger Swiss Ramble said on the subject in 2015. Does it sound familiar?

“One of the most important issues for Manchester City has been FFP. Although the club believed that it had complied with these regulations, there was “a fundamental disagreement between the club’s and UEFA’s respective interpretations of the FFP regulations on players purchased before 2010.” Basically, the club thought that it would have been able to exclude £80 million of such costs from its break-even calculation, but this was not allowed, as the break-even deficit in 2011/12 was not entirely due to pre-June 2010 player contracts. The difference was negligible, but this meant that the entire £80 million could not be utilized.

Although City felt that the goalposts had been moved after the game had started, notably due to a 2013 change in UEFA’s guidance notes, they decided to draw a line under the matter and not contest the ruling in the courts.”

If you want to check yourself, it’s here: http://swissramble.blogspot.com/2015/01/manchester-city-roll-with-it.html in the fifth and sixth paragraphs from the end.

So, it’s not just me saying this (and there was no collaboration between us on this). As Herr Klopp would say: “Boom!”

In hindsight, UEFA might have done City a big favour. Imagine if they hadn’t changed the key test for assessing the impact of those pre-June 2010 wages? City might have been able to claim mitigation under Annex XI and avoid sanctions.

Had they done so, UEFA might have some justification to re-open the matter and the howls of outrage would be deafening, knowing City had used potentially dubious methods to escape punishment.

But it’s important to point out that UEFA appear to have known what we’d done, having commissioned PWC to report on it. It’s not apparent that we hid anything from them.

But by imposing the sanctions, with City having failed to be able to use Annex XI, there may be no point in revisiting the matter or any desire to do that.

After all, does it really matter if they failed FFP by £76.8m or £100m?

Summary

I appreciate that this has been a long and probably very dry read so I’ll summarise it with some bullet points:

- City had aggregate losses of £150.3m in the two years assessed in the first monitoring period.

- £98.7m of that was incurred in 2012 and £51.6m in 2013.

- There were £35m of expenses that could be deducted and I’ve assumed that’s £17.5m in each of the 2012 & 2013 financial years.

- City’s Aggregate Break-Even Deficit was therefore £115.3m split £81.2m in 2012 and £34.1m in 2013.

- The acceptable deviation (our maximum allowable loss) was £38.5m (which is €45m at the May 2013 exchange rate).

- City were therefore £76.8m adrift of meeting that, meaning they would fail the first assessment by a wide margin.

- They needed to use the Annex XI(2) provision to escape punishment if they could.

- There was a potential ambiguity in the wording of that Annex XI(2) clause.

- In the original version of the crucial test, City had to show those £80m wages were fully responsible for the £76.8m deviation from the maximum acceptable deviation, which they were.

- After the publication of their 2012 accounts, in Feb 2013, this test was changed.

- The new test meant that City had to show that the £80m wages fully covered the 2012 break-even deficit, which was £81.2m. It didn’t by a narrow margin (£1.2m).

- City therefore not only failed FFP but couldn’t use the Annex XI(2) mitigation clause and faced sanctions as a result.

I therefore feel confident that I’ve proved, using UEFA’s own documents, that:

- UEFA changed the crucial test for pre-June 2010 wages.

- City would have met the original test as set out in the 2011 toolkit.

- The change meant that city didn’t meet the revised test, which led to them being sanctioned.

You can therefore see why City wouldn’t have been happy and probably felt they had a good case to go to court. The question is, did UEFA do this deliberately, knowing that once City’s 2012 accounts were set in stone, they had a target to aim at? Or was it just a change to make the test fit with what they intended by the FFP wording? There’s no evidence, other than the timing, that the change was deliberate.

But, if it was, UEFA certainly wouldn’t want to go to court over it. Even if it wasn’t. City could still try to argue around UEFA’s interpretation of the requirement as set out in the FFP regulations.

In the light of the Football Leaks story though, would City really want to go to court, knowing there was a question mark over some of their revenue and that they’d done things that UEFA were dubious about and might well challenge? A settlement suited both parties therefore.

The concern must be whether meeting the break-even targets set in the sanctions (which they did) was achieved by methods that might be regarded as against the spirit of the FFP rules. But, as I said above, would UEFA really want to go there?

I hope this rather involved, long and complex piece has helped you understand what I believe was the key reason why we ultimately failed FFP. If you lasted the course and understood it then it’s been worth my while writing it.

This Article was written by Colin Savage (@PrestwichBlue) From The BoltFromTheBlue Website: boltfromtheblue.live. All credit and rights remain with the author.